Are Premier League clubs sufficiently anchored for the next wave of financial regulations?

UCFB academic Chris Winn has been writing about the Premier League clubs and how they are affected by financial regulations in the modern football world.

Here’s what Chris, course leader for MSc Football Business, had to say:

Never before have financial regulations gained so much airtime in the world of English football. The last year has brought the concepts of profitability, amortisation and allowable expenditure into day-to-day fan vernacular, with fans now debating the sale of academy talent not from a tactical viewpoint, but their ability to generate ‘pure profits’ and as such alleviate the risk of points deductions. As a football finance expert, a world I certainly never saw coming!

However, with so many updates, tweaks, changes and challenges to financial regulations in the last year, it’s easy to get lost in terminology.

For a start, ‘Financial Fair Play’ no longer even exists, and yet is often incorrectly used as an umbrella term for all things financial regulations in football. And the recent announcement by the Premier League that 80% of clubs had backed the principle of a salary cap as of the 2025/26 season led to some declaring this meant the onset of a world where clubs further down the Premier League would be able to spend to their hearts’ content, when reality is far different.

With changes almost certainly on the horizon in some guise, the following analysis looks to provide a clear picture of what is to come, and the extent to which Premier League clubs are sufficiently anchored for the next wave of financial regulation.

Where are we now?

Since 2013/14, the Premier League has operated the Profitability and Sustainability Regulations, which regulate clubs on their ‘adjusted’ profit before tax over a rolling three-year period. Clubs are allowed to ‘adjust’ their profits by adding back amounts spent on items such as infrastructure, youth football and women’s football; items that are deemed to contribute to long-term sustainability. Consistent Premier League clubs are allowed to ‘lose’ up to £105m over three seasons, provided all but £15m of said losses are ‘securely funded’ by equity contributors.

Where next?

Following recent cases of club breaches, coupled with Premier League losses before tax reaching £722m in the 2022/23 season, it has been widely reported that the Premier League is set to impose a new set of financial regulations from 2025/26, directly regulating clubs’ expenditure on player wages, player amortisation, and agent fees (‘total spend’) as a proportion of their revenue (‘total income’). Indeed, this same mechanism was recently adopted by UEFA as part of their new Financial Sustainability Regulations for clubs in European competition, commonly known as the ‘Squad Cost Control Rule’ (‘SCCR’).

Under UEFA’s regulations, clubs in European competition are currently in a transition phase, gradually working towards the imposition of a 70% ratio in this regard by 2025/26. Their regulations work on a calendar year basis and allow for profits on player sales prorated over three years as part of the calculation.

The Premier League are reportedly planning on imposing a similar calculation, albeit likely over a season, and the extent to which profits on player sales would be incorporated has not been openly communicated. Clubs not in European competition would be allowed to spend up to 85% of their total income on player related expenditure, whilst clubs in European competition would align with the UEFA rules at 70%.

What about the salary cap?

The salary cap that was recently announced as being under consideration by the Premier League would be complimentary to the above SCCR, as opposed to being instead of it. Designed to ensure that the existing revenue gap between the top and bottom of the Premier League does not equate to further disparities in the ability to sustainably invest in playing squads, the proposed ‘cap’ is rumoured to be 4.5-5 times the smallest Premier League central distribution in a given season- a concept known as ‘anchoring’. In the 2022/23 Premier League season, the club that received the lowest Premier League central distribution was Southampton at £103.6m; if implemented on this basis, this would result in a player expenditure cap of £466m- £518m depending on the level chosen.

Given 2022/23 was the start of the current three-year Premier League broadcast cycle, 2025/26 would mark the commencement of the next broadcast cycle, which will be set at four years. Whilst the domestic deal has been finalised at a 3% uplift on the current cycle, the international packages are yet to be finalised, though the latter has shown significant growth over time. A total rights uplift of 10% isn’t out of the question, which may increase the cap to £512m-£570m dependent on level chosen.

Are clubs ready for the new regulations?

The nature of club financial reporting means that the latest set of financials that we have available for all clubs is 2022/23, with two more rounds of financials to come before the onset of the new financial regulations.

Nevertheless, a picture can very much be painted of how ready Premier League clubs are for the changes ahead.

Whilst not entirely the case, the following analysis assumes that player agent fees are capitalised in full as part of player acquisitions, and as such form part of the annual amortisation expense. Furthermore, in the 2022/23 season, the clubs that participated in European competition were Man Utd, Man City, Arsenal, Chelsea, Liverpool, Tottenham and West Ham – and therefore would have the 70% restriction applied that year as opposed to 85%. Finally, financial accounts do not distinguish between player and non-player wages- as such the full totals have been utilised.

Three scenarios have been analysed:

Scenario 1 applies a salary cost control rule that incorporates the profits on player sales for the given season (2022/23);

Scenario 2 applies a salary cost control rule that incorporates a three-year average of profits on player sales (akin to the UEFA approach); and lastly,

Scenario 3 applies a salary cost control rule that only utilises revenues, with no profits on player sales added in at all.

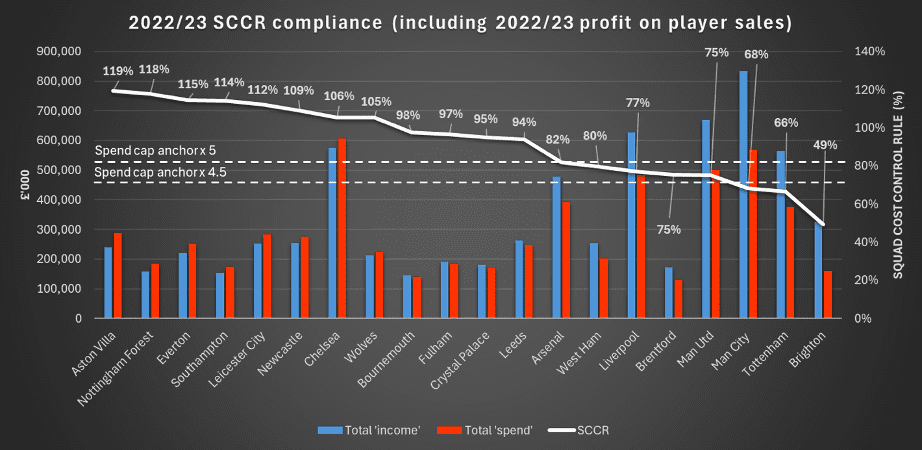

Scenario 1: SCCR with annual profit on player sales

Scenario 1 demonstrates the relationship between the ‘total income’ (including 2022/23 profit on player sales) and total player related expenditure for all 2022/23 Premier League clubs. The two possible levels of expenditure cap (based on the central amount received by Southampton in 2022/23) are illustrated by the white dotted lines.

Whilst eight clubs come in under the maximum 85% SCCR level, four of these (Arsenal, West Ham, Liverpool and Man Utd) participated in Europe that season but were above 70%. As a result, only four clubs would have adhered to the SCCR that season under this scenario. When an expenditure cap is also put in place, Man City would also fall foul of the regulations- leaving just Brentford, Tottenham and Brighton as clubs operating within the full remit of the regulations.

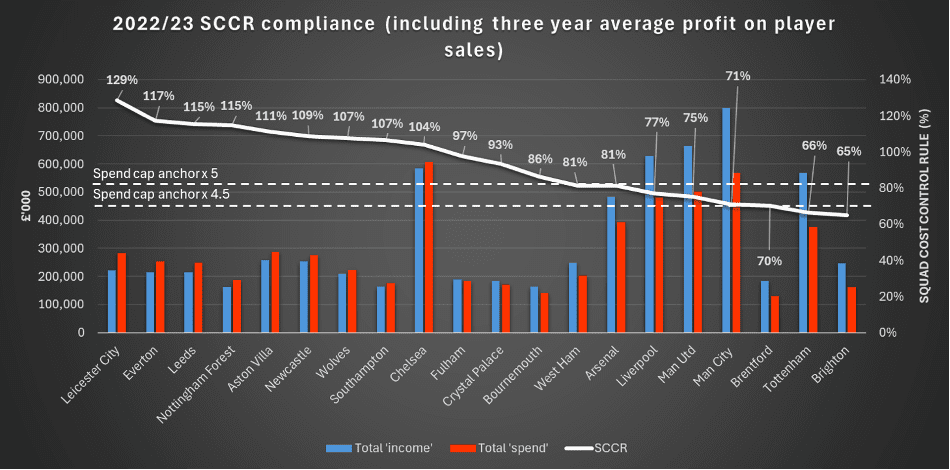

Scenario 2: SCCR with three-year average profit on player sales

Scenario 2 encapsulates a three-year average of profit on player sales in calculating total income. This matches to UEFA’s methodology and allows for the inconsistencies of player trading on an annual basis.

Despite this, the same eight clubs come in under 85%, this time five of them being European participants in excess of 70%. Regardless of the expenditure cap, the same three clubs demonstrate compliance, these being Brentford, Tottenham and Brighton.

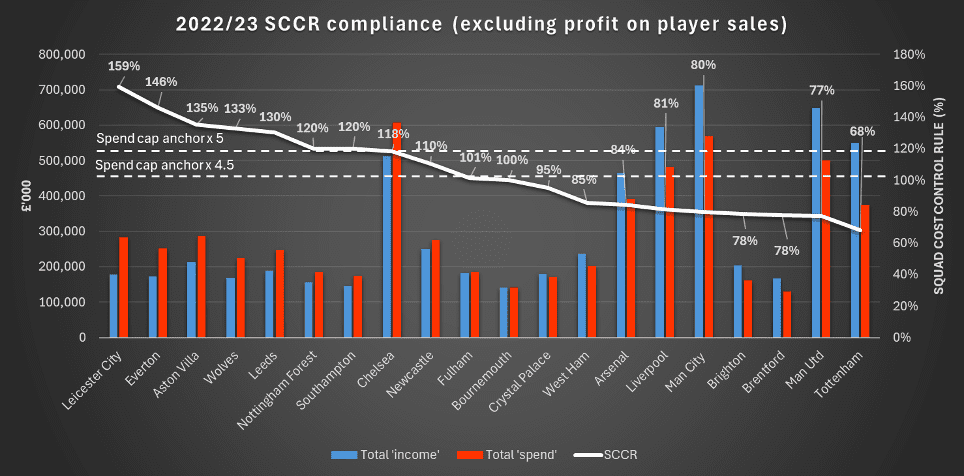

Scenario 3: SCCR excluding profit on player sales

Scenario 3 removes the inconsistency of profits on player sales and allows only for clubs’ operational revenues as the basis of the SCCR formula.

Despite this, the same eight clubs come in at or under 85%, with Brentford, Tottenham and Brighton the only teams to again comply with the regulations once European football has been accounted for.

Of course, it should be noted that clubs are currently planning with regards to the Profitability and Sustainability Rules rather than a version of SCCR with an associated expenditure cap, but per this analysis, 17 (85%) of the 20 2022/23 Premier League clubs would not be ready for the changes ahead based on European participation that season, regardless of the scenario employed.

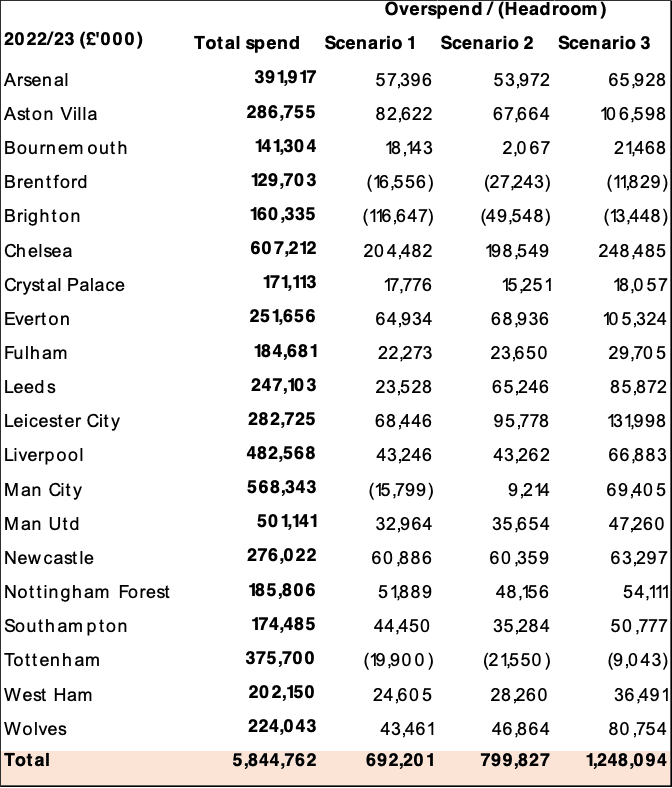

The table below summaries the overspend (or in isolated cases headroom) of each club when applying the SCCR alone in 2022/23, under each of the three scenarios:

As demonstrated, depending on the measure applied, Premier League clubs were collectively c.£690m – £1.25bn in excess of the levels of player expenditure that would be allowed, relative to income generated, in 2022/23.

Does the proposed expenditure cap make a difference?

Based on 2022/23 figures, only four clubs incurred levels of player expenditure in excess ofeither the 4.5x or 5x cap (as demonstrated by the white dotted lines in the charts), these being Chelsea (£607m), Man City (£568m), Man Utd (£501m) and Liverpool (£483m). This partially explains the two Manchester clubs voting against the proposition, and Chelsea abstaining.

However, under Scenario 1 (annual profits on player sales included), Chelsea and Liverpool exceed the SCCR threshold (106% and 77% respectively). Were they both to theoretically comply, their levels of player expenditure would fall underneath the proposed cap levels. Man Utd (75% SCCR) would still breach a 4.5x cap if they reduced their SCCR ratio to 70%. Man City (68%) comply with SCCR, but would be £50m in excess of a 5x cap at this level of spend.

Under Scenario 2 (three-year average of profits on player sales included), Chelsea (104%), Liverpool (77%), and Man Utd (75%) would all fall underneath the proposed cap levels if they were to theoretically comply with the SCCR limit of 70% for European clubs. Man City however (71%) would still be £41m in excess of a 5x cap were they to drop their levels of expenditure to a 70% SCCR in this scenario.

Lastly, under Scenario 3 (profits on player sales excluded), Chelsea (118%), Liverpool (81%) and Man Utd (77%) would again all fall underneath the proposed cap levels if they were to theoretically comply with the SCCR limit of 70% for European clubs. Man City (80%) would come in under a 5x cap if they were to drop their levels of expenditure to a 70% SCCR, butwould still exceed a 4.5x cap by £33m.

Pulling up the anchor

To conclude, the numbers appear to indicate that Brentford, Tottenham and Brighton are the only Premier League clubs (based on 2022/23) with business models ready for the changes ahead (allowing for the specifics of European participation in 2022/23). Regardless of the scenario that plays out, Man City appear to have the most to lose in terms of the relative size of their resources vs allowable spend under the proposed new regulations.

Whilst it remains to be seen how high the anchor will go, or indeed if a transitional phase will be implemented, it’s clear that this new set of regulations will remove a lot of the subjectivity which has impacted the Profitability and Sustainability regulations to date.

You may also be interested in

Books

Sports Coaching, Physical Education & Performance Analysis

Reflective Practice

View Research

Academic Journal Articles

Sports Coaching, Physical Education & Performance Analysis

Identification and assessment of perceptual-cognitive skills in academy soccer

View Research

Industry Reports & White Papers

Business, Finance & Law

The Fair Game Vision for a Football Governance Bill. Fair Game.

View Research

Our Partners